Cash operating cycle and the related areas

In this article, we will go through the cash operating cycle, working capital cycle and the related subject areas. Such as managing inventory, managing receivables and managing payables.

Working capital cycle is the period which laps between payment collection from customers and the payment made to the supplier. Working capital cycle some times called a cash operating cycle, trading cycle, cash conversion cycle.

How to calculate the working capital cycle ( cash operating cycle) ?

We can calculate the working capital cycle in the following manner,

- The average time that raw materials remain in inventory

- Less the period of credit taken from suppliers

- Plus the time taken to produce the goods

- Plus the time taken by customers to pay for the goods

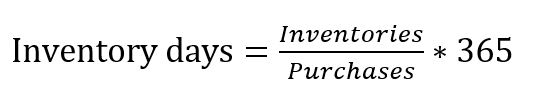

Similarly, this equation can be used to calculate the cycle . inventory days + receivables days – payables days where,

Managing inventories

There are three main costs associated with inventories.

- Purchasing cost

- Ordering cost

- Holding cost

As the finance manager, you can calculate the total cost of inventories by totaling up the above-stated costs. But how do we know the best ordering quantity at a time? This is one of the crucial elements of inventory management. This element is known as the economic order quantity (EOQ) model.

The economic order quantity (EOQ) model is the technique where to decide the optimum order size for inventories, which will minimize the costs of ordering inventories plus inventory holding costs.

Managing accounts receivable

As you well aware of many businesses maintain separate ledger for accounts receivables.Offering credit comes at a cost: the value of the interest charged on an overdraft to finance the credit period, or loss of interest in cash has not been received and deposited in the bank. An increase in the benefit of the additional sales resulting credit supply could offset this cost.

How to manage account receivables effectively?

Regular monitoring of accounts receivable is very important. Apart from that following technique can be used to manage receivables effectively.

- Customer history analysis.

- In-house credit ratings for customers.

- Maintaining aged accounts receivable listing.

- Credit utilization report.

- Early settlement discounts schemes are also another best option to manage debtors.

Factoring

Companies use factoring and invoice discounting to help short-term liquidity or to reduce administration costs.

Invoice discounting

This helps to raise working capital, and in this method, trade receivables of a company purchase at a discount price.

Debt defeasance

Arises when a company wants to redeem a bond or a loan but does not incur prepayment penalties. Remaining deposit the payment obligations are transferred to a third party, as well as sufficient assets (such as cash or bonds) to meet these obligations.

Managing accounts payable

Effective management of accounts payable trade is to seek satisfactory credit terms from suppliers, get credit in times of liquidity shortage, and maintain good relations with suppliers.

The following technique can be used to manage account payables effectively.

- Obtain satisfactory credit.

- Attempting to extend credit.

- Maintaining good relations with important suppliers

{kind=link}