Cost of capital

In this article, we will look at the concept of cost of capital that can be used as a discount rate in evaluating a firm’s investment. We first base the cost of equity calculations on the dividend valuation model. Then, we will look at a method of establishing the cost of risk-taking stocks: the capital asset pricing model. Besides, we will go through the cost of debt calculations and WACC weighted average cost of capital calculations in detail.

Investment decisions, financing and the cost of capital

The cost of capital

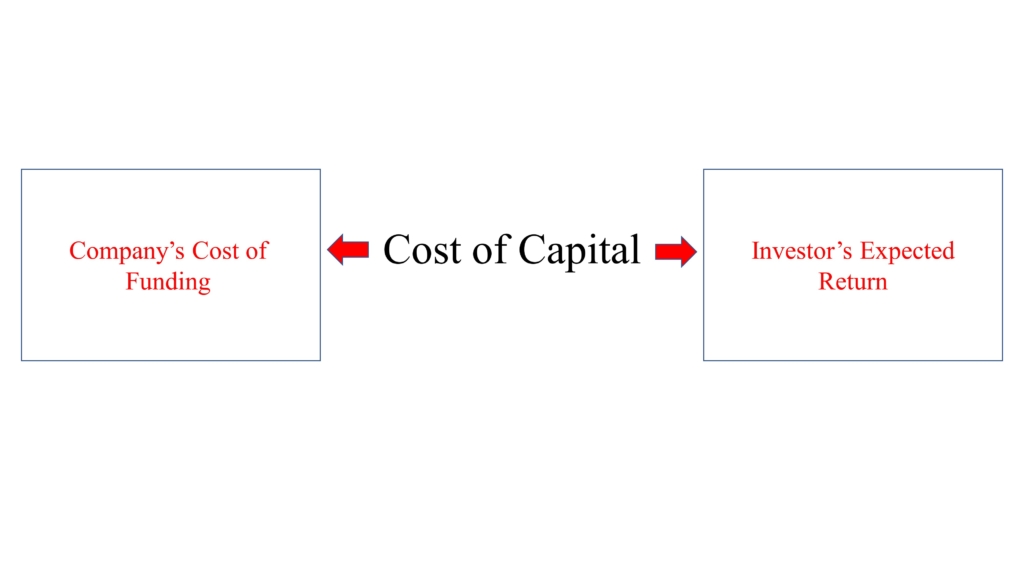

Therefore, the cost of capital is the minimum the company must earn to pay for their investors. The computed COC will use in investment appraisal as the discount rate.

The cost of capital as an opportunity cost of finance

Cost of capital is referred to as the opportunity cost of finance from the investor’s side. If they do not get the return that they expect from investing in our company, most probably they will look for another investment. For instance, if a bank lends for the company, the expected minimum return/yield is the interest cost. So, the opportunity cost would be the return they that could have gained through lending for another company. Therefore, COC is the opportunity cost the bank has given up.

This concept is the same as from the investor’s side as well; the company has to pay a sufficient amount to keep the investors happy. Otherwise, they would sell their shares and divest in the company. So, the opportunity cost for the investor is that the yield that would have been earned from investing somewhere.

The cost of capital and risk

- Risk-free rate – This is the yield on government securities

- The premium for business risk – This is the return required to the risk existed on the business and the uncertainty about the firm’s business prospects.

- The premium for financial risk – This risk is related to the higher debt level of the company. In other words, when the company is increasing its gearing level, they will have to pay a higher interest portion from the EBIT. However, this will result in a low level of earnings for the investors as dividend payments.

Cost of Equity

There are two methods for calculating the cost of equity. If you are not familiar with cost of equity yet, we would recommend checking our “Cost of Equity “article again.

- Dividend valuation model

- The capital asset pricing model

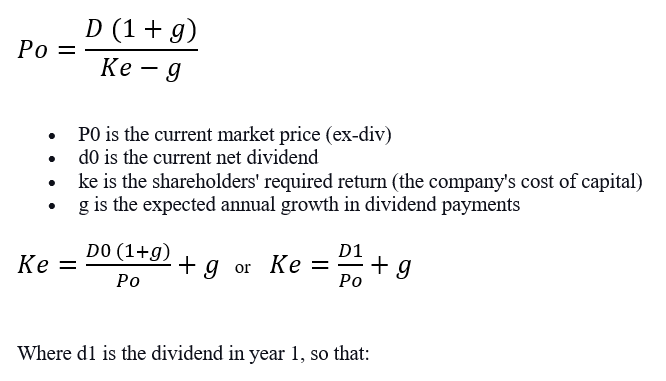

Dividend valuation model / The Gordon growth model

There are two aspects of the dividend, namely cum dividend and ex-dividend. Cum dividend means, the purchaser has the right to receive the next dividend. However, Ex-dividend means that the purchaser of shares is not entitled to receive the next dividend payment.

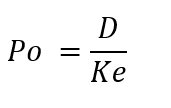

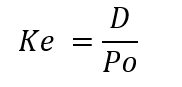

If the dividend per share is constant in the future, the following equation can be used to calculate the Ex-dividend price.

- Po = Ex-dividend price

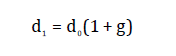

- Ke = Shareholders required return

- D = Constant annual dividend per share

We can use the above formula to calculate the cost of equity easily.

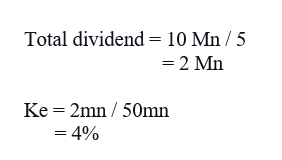

Dividend valuation model example

Miles Inc has a dividend cover ratio of 5.0 times and expects zero growth in dividends. The company has one million Rs. 1 ordinary share in issue and the market capitalisation (value) of the company is Rs. 50 million. After-tax profits for next year are expected to be Rs. 10 million.

Required – Calculate the expected rate of return from the ordinary shares.

Solution

Dividend growth model formula

Shareholders always prefer to have a growth in their dividend year by year and not receiving the constant dividend for perpetuity. Therefore, the following formula can be used to calculate the price of a share and the cost of equity. (Assume dividend growth)

Ex-dividend share price

Ex-dividend share price can be calculated taking the present value of future dividend earnings. However, we assume that the dividend growth rate is constant for perpetuity.

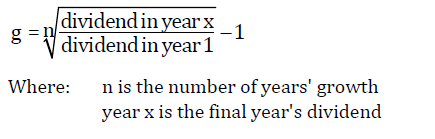

Estimating the growth rate

There are two methods that we can estimate the growth rate.

- Historic growth – you can analyze the past trends and determine the growth rate of a dividend.

- Current re-investment level – You can use current reinvestment level to determine the growth rate as well.

g = br

- b- Retained profits portion

- g- Annual growth

- r – Yield on new investment

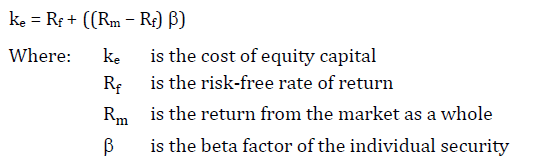

The capital asset pricing model (CAPM)

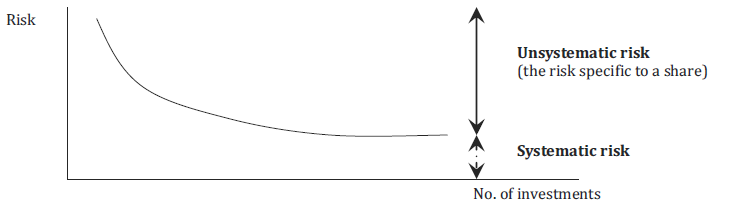

CAPM is another way of calculating the cost of equity of a firm. This model incorporates risk. Also, There are two types of risk involved in CAPM.

- Systematic risk – This is also called an inherent risk. When an investor invests in the company, there will be some risk involved with it. Sometimes the actual yield may differ from the expected return. Therefore, Systematic risk is not avoidable. Similarly, systematic risk arises due to the business risk and the financial risk with each investment.

- Unsystematic risk – Investors can reduce this risk by having a diversified investment portfolio. More you invest, the more you can reduce the risk of unsystematic risk.

Systematic risk and unsystematic risk: implications for Investments

- If an investor wants to avoid the risk 100%, they should invest in government securities.

- If the investor holds shares in few companies, he will face for the unsystematic risk. However, having a balanced portfolio will only be exposed to systematic risk.

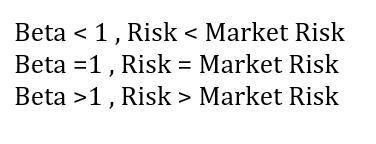

The beta factor

This is the best measurement of systematic risk an investment. CAPM is mainly focused on how systematic risk affects returns and share prices. Therefore, the beta factor is a valuable learning point in corporate finance.

CAPM formula

The market risk premium

This is the difference between the return on the shares as a whole in a market and the return from the risk-free investment. (Rm – Rf )

Capital asset pricing model (CAPM) theory includes the following propositions.

- Investors concerned about the returns; they require a return over the risk-free rate.

- Investors should not require a premium for the unsystematic risk. Hence this risk can be diversified away by holding a wide range of investment portfolio.

Problems with applying the CAPM in practice

- There are problems in determining the excess return (market risk premium).

- Determine the risk-free rate (risk-free rate is taken for government security which is not always true). The interest rate varies with the terms of lending.

- There may be errors in calculating the beta factor.

- CAPM is also unable to forecast returns accurately.

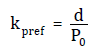

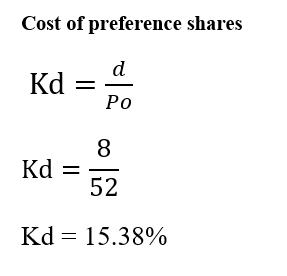

Cost of preference shares

Preference shares are also part of the company’s source of financing. Therefore, when calculating the cost of capital preference, share cost will also be considered.

- P0 is the current market price of preference share capital after payment of the current dividend.

- D is the dividend received.

- Kpref is the cost of preference share capital.

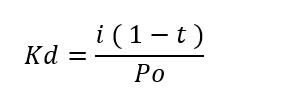

The cost of debt

Cost of debt is always lower than cost equity. The reason behind the lower cost is the tax benefits that can be obtained through debt. However, there are different techniques we can use to determine the redeemable and irredeemable debt.

Cost of irredeemable debt

Irredeemable debt only has the interest rate, and investors can earn from interest to perpetuity.

Cost of irredeemable debt formula

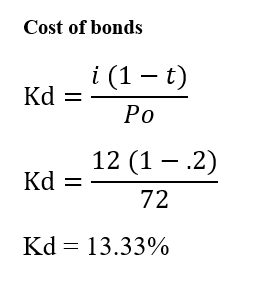

(kd) Cost of irredeemable debt capital, paying interest i in perpetuity, and having a current ex-div price P0.

Cost of redeemable debt

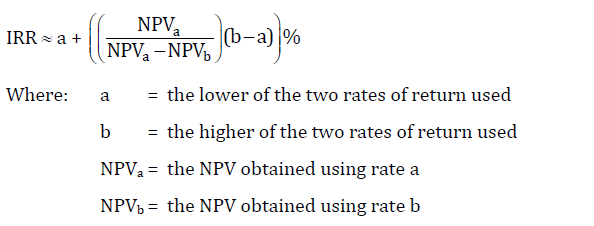

If the debt is redeemable, the investor will get both interest and capital amount invested at the end of the redemption date. IRR method will use to calculate the cost of redeemable debt. IRR is the discount rate at which NPV becomes zero means neither investor nor company would gain.

Cost of redeemable debt formula

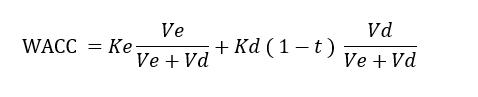

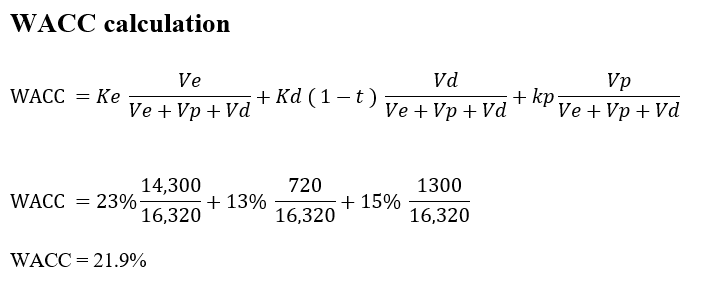

The weighted average cost of capital / WACC

We have looked at different types of cost calculations based on the financing methods. How does this help us to adjust the discount rate to apply for capital valuation or discount cash flow (DCF) investment appraisals as a whole? We now need to calculate the weighted average capital cost (WACC), which combines the costs of two or more types of capital.

How to calculate WACC?

WACC is the average cost of a company’s financing (equity, debt and bank loans). However, weighing is usually based on market valuations, current yields, and after-tax costs.

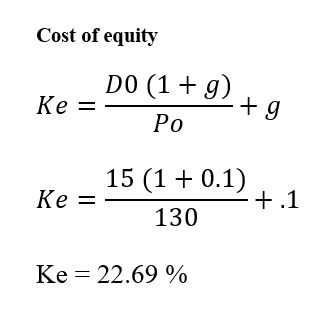

WACC example

An entity has the following information in its statement of financial position.

| $ | |

| 50,000 ordinary shares | 5.500 |

| 8% preference shares of $ 100 each | 2.500 |

| 12% unsecured bonds undated | 1.000 |

The ordinary shares are currently quoted at $ 130 each, the bonds are trading at $ 72 per $ 100 nominal and the preference shares at $ 52 each. The ordinary dividend of $ 15 has just been paid with an expected growth rate of 10%. Corporation tax is currently 20%.

Required – Calculate the weighted average cost of capital for this entity.

Solutions – Market values

| $ (Mn) | ||

| Equity ( Ve) | 5.500/50 x 130 | 14,300 |

| Preference Shares (Vp) | 2500/100 x 52 | 1,300 |

| Bonds (Vd) | 1000/100 x 72 | 720 |

| Total Market Value | 16,320 |

Assumptions to take WACC as DCF in investment appraisal

- New investment should finance by a new source of funds.

- Cost of capital should reflect the marginal cost.

- WACC reflects the company’s long-term funding cost.

Arguments against using the WACC

There are few arguments against using WACC as the cost capital of investment.

- If a company undertakes a new investment, it may have a different business risk that of the existing business. Therefore, using the calculated WACC is not fit.

- When the company raise new funds, capital structure may change. Therefore, the financial risk for the existing shareholders may change. Thus, previously calculated WACC is not suitable.

The marginal cost of capital approach

The marginal cost of capital approach

This marginal cost of capital approach is the calculation of the marginal cut-off rate for acceptable investment projects.

{kind=link}